Why This Comparison Matters Now

Global bond markets are the backbone of institutional investing — funding governments, corporates, and infrastructure projects worldwide. Yet, despite their scale, bond markets still rely on processes that were designed decades ago: manual reconciliation, delayed settlement, fragmented intermediaries, and limited investor reach.

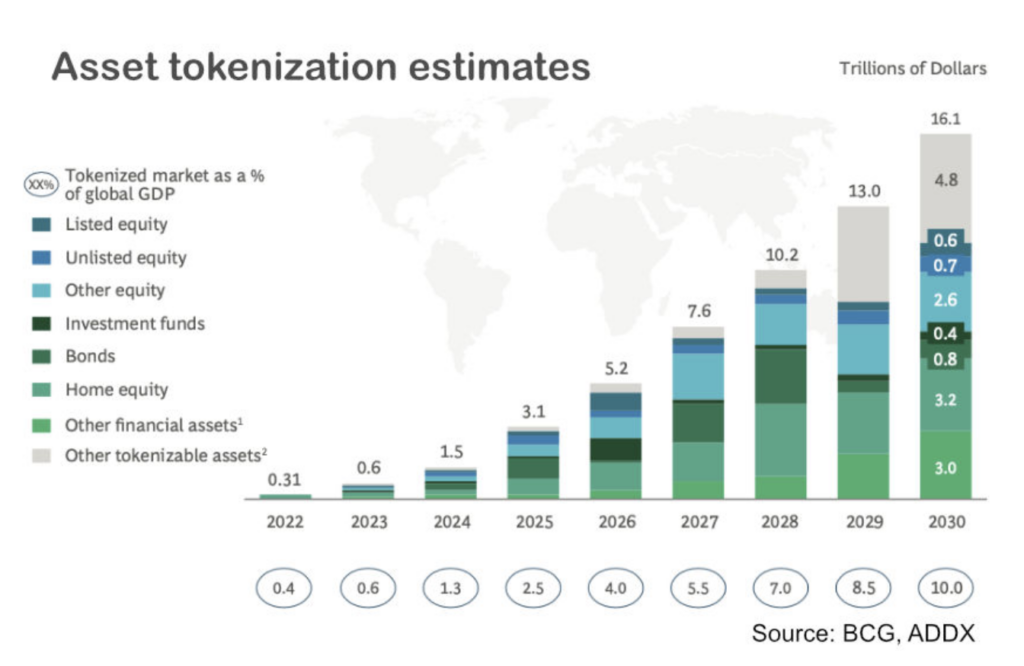

Over the last few years, tokenized bonds have emerged as a credible alternative issuance and distribution model. What started as pilots is now moving into live issuance by asset managers, banks, and public institutions.

For institutional investors, the question is no longer “What is tokenization?”

It is “How does a tokenized bond differ from a traditional bond — and why does it matter?”

What Is a Traditional Bond?

A traditional bond is a debt instrument issued through capital-market infrastructure involving Issuers (government or corporate), Arrangers and dealers, Central securities depositories, Custodians and clearing houses

Ownership records, settlement, and servicing are handled through multiple intermediaries. Settlement typically occurs on a T+1 / T+2 basis, and participation often requires large minimum ticket sizes.

This model is reliable — but slow, expensive, and operationally heavy.

What Is a Tokenized Bond?

A tokenized bond represents the same economic instrument — principal, coupon, maturity — but is issued and managed digitally using blockchain infrastructure.

Instead of relying on multiple layers of reconciliation, here the ownership is represented by digital tokens, transfers and settlement occur on a shared ledger, cash flows (coupons, redemption) can be automated.

Importantly, the underlying asset is still a bond — tokenization changes how it is issued, distributed, and serviced, not the credit risk itself.

Traditional Bonds vs Tokenized Bonds – Side-by-Side

Core Structural Differences

| Aspect | Traditional Bonds | Tokenized Bonds |

| Issuance process | Multi-party, document-heavy | Digitally structured, streamlined |

| Settlement | T+1 / T+2 | Near-real-time |

| Minimum investment | High (often $100k+) | Fractional, flexible |

| Ownership records | Fragmented across systems | Single shared ledger |

| Market access | Mostly regional | Global, 24×7 capable |

| Servicing | Manual reconciliation | Automated via smart logic |

What This Means for Institutional Investors

Instead of shifting between perspectives, here is a clear investor-centric view.

| Area | Traditional Bonds | Tokenized Bonds |

| Operational efficiency | High back-office effort | Reduced processing & reconciliation |

| Liquidity access | Limited trading windows | Potential for always-on markets |

| Transparency | Periodic reporting | Near real-time visibility |

| Portfolio construction | Large ticket constraints | Granular allocation possible |

| Cross-border investing | Complex and slow | Digitally native, faster |

| Cost structure | Multiple intermediaries | Leaner issuance & servicing |

In simple terms: tokenization does not change the bond’s risk — it improves the infrastructure around it.

Why Institutions Are Exploring Tokenized Bonds

Across global markets, institutions are adopting tokenized bonds for three practical reasons: First one is Efficiency that means faster settlement, fewer intermediaries, and automated servicing reduce operational friction. Second is Access & Flexibility i.e. fractionalization enables better portfolio construction and broader investor participation. Third is Future-ready Infrastructure as tokenized instruments are easier to integrate with digital custody, programmable cash flows, and next-generation trading venues.

How the Market Is Evolving

One of the most important changes is the shift in mindset. Tokenization is no longer viewed as a replacement for traditional capital markets, but as a modern delivery layer for the same financial instruments. Bonds are still issued, rated, and underwritten in the same way — what changes is how they are issued, settled, serviced, and distributed. This distinction has made tokenization more acceptable to institutional investors, compliance teams, and regulators.

Another key evolution is the maturing of supporting infrastructure. Custodians, compliance providers, legal firms, and technology vendors are now capable of supporting digital securities in a regulated manner. Settlement models are moving closer to real-time, reporting is becoming more transparent, and cross-border participation is easier to manage. This ecosystem readiness is critical, because tokenized bonds only scale when all parts of the lifecycle are institution-grade.

Finally, market focus is shifting toward practical use cases. Instead of broad experimentation, institutions are prioritising areas where tokenization delivers immediate value — such as private credit, structured debt, short-duration bonds, and asset-backed instruments. Over time, as secondary trading venues mature and standards emerge, tokenized bonds are expected to coexist with traditional bonds and gradually become the preferred format for certain segments of fixed income instruments.

Where Vayana Digital Assets Platform (VDAP) Fits In

The transition from traditional bonds to tokenized bonds requires more than blockchain technology — it requires a complete operating framework that financial institutions can trust. This is where the Vayana Digital Assets Platform (VDAP) plays a critical role.

VDAP is designed as a modular, end-to-end tokenization infrastructure that supports the full lifecycle of tokenized bonds and private credit instruments. It enables issuers to structure and launch digital debt products while ensuring that regulatory, legal, and compliance requirements are embedded from day one. Instead of institutions stitching together multiple vendors for issuance, compliance, custody, and distribution, VDAP brings these capabilities together on a single platform.

For institutional investors, VDAP provides a structured and transparent environment to access tokenized bonds. Investor onboarding, eligibility checks, and compliance controls are integrated into the platform, while coupon payments, redemptions, and reporting are automated through digital workflows. This reduces operational friction and improves confidence in participating in tokenized fixed-income products.

From an institutional strategy perspective, VDAP acts as a bridge between traditional capital markets and digital asset infrastructure. It allows banks, asset managers, fintechs, and platform providers to launch and scale tokenized bond programs without re-architecting their existing systems. As tokenization moves from early adoption to mainstream implementation, VDAP enables institutions to participate in this evolution in a compliant, scalable, and future-ready manner.

Conclusion

Traditional bonds are proven. Tokenized bonds are evolving the same asset class for a digital, global, always-on financial system.

For institutional investors, the decision is not about choosing one over the other — it is about when and how to adopt tokenized infrastructure to gain efficiency, transparency, and future readiness.

Tokenization will soon stop being a differentiator.

It will simply become how bond markets operate.